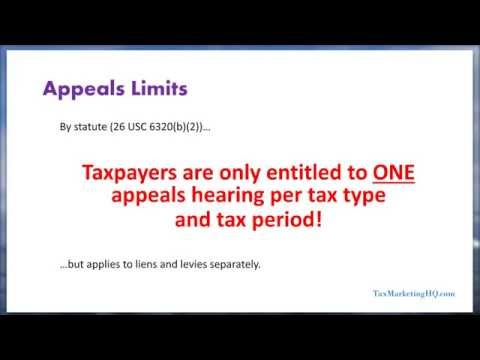

Good morning, my name is Jason Bowman and welcome to this month's continuing education webinar. Today we are going to be talking about the collections due process appeal program. The collections new process appeal is one of the most powerful tools in your tax resolution arsenal, and that's why I wanted to start with this particular topic for our first technical webinar. So glad that all of you could be with us. This release is scheduled to last an hour. I will try to finish it within the hour, but it's not uncommon for me to go long on these, so I will try to within the hour. But I've got a lot of stuff I want to cover here. So the way that this is going to work, the IRS requires me to check occasionally to make sure that everybody is still awake, so for the continuing education credits, a couple of times throughout the hour I will throw up a review question that will show up as a poll. Just answer the poll question. That will mark your attendance, basically, and that you're still awake. Our course objectives today are to talk about the purpose of the CDP appeal program. I will discuss why you want to use it. We'll discuss your client's eligibility for the program. I'll talk about forms. We'll talk about how the hearings go, the IRS personnel that are involved. We'll talk about some Appeals outcomes - you know what comes out the other end of this whole thing. So the first question, why would you want to file a CDP? This answers the question as to why this is such a valuable tool for us as practitioners. The collections due process appeal provides a state of enforcement, and what that means is that for the tax periods...

Award-winning PDF software

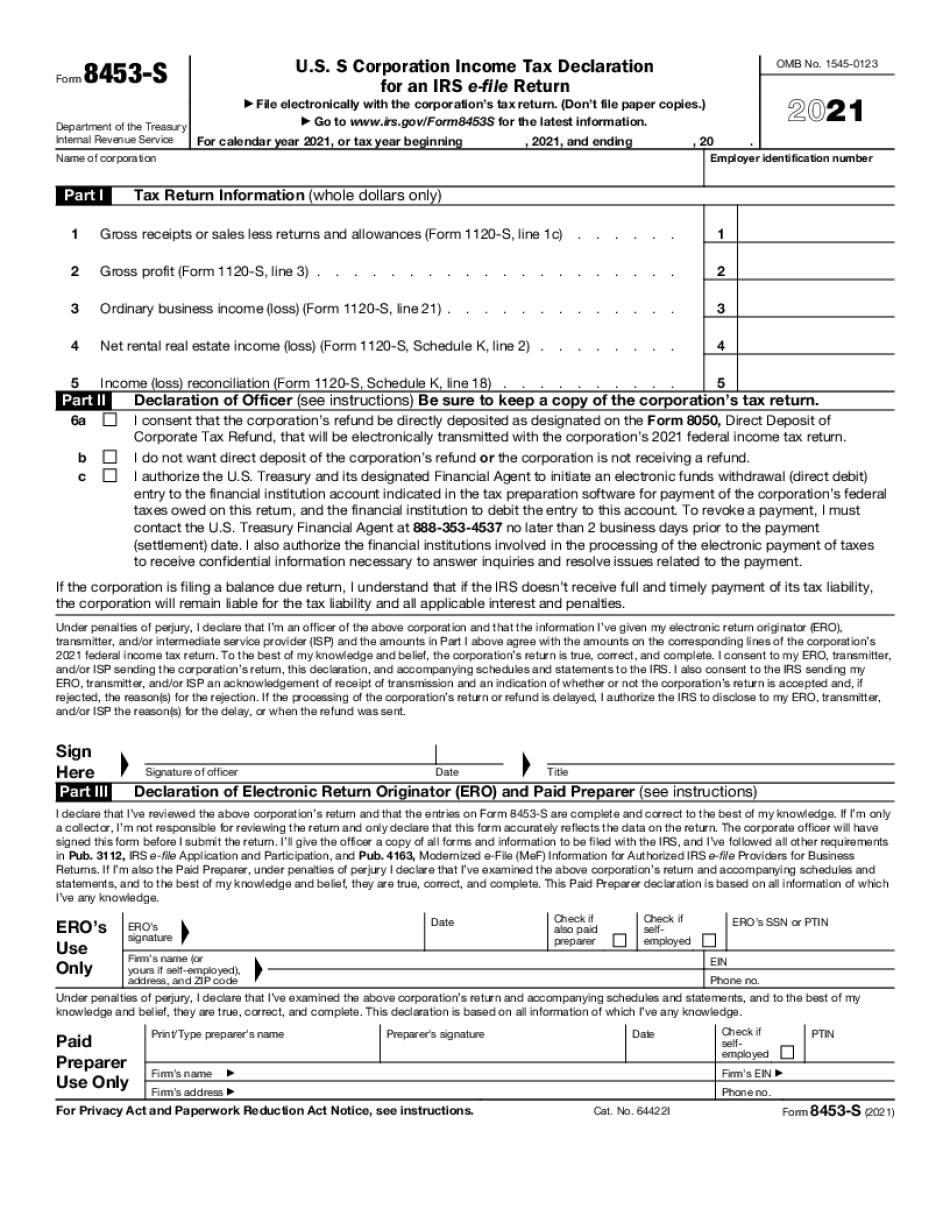

Video instructions and help with filling out and completing Can Form 8453 S Taxpayer