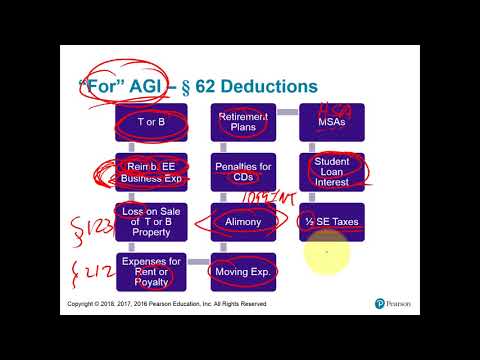

A class, this is our video lecture for chapter number 6 part 1. We are going to be calculating deductions and losses, and seeing what limitations there are in trying to claim them. If you remember, in past chapters, we were talking about income and the general rule is that all income is going to be taxable unless specifically excluded or treated tax-free. So the mirror image is that deductions, our column expenses, are not deductible unless specifically allowed by the law. So maybe it's the worst of both worlds here. It says everything is taxable income and here it says everything is not deductible unless it's specifically excluded or allowed as a deduction. Here you can see deductions can be classified maybe into three broad categories. This first one here, which is probably the best of the three for at least for tax purposes, is called trade or business expenses under this section. It's a real broad topic, generally any type of costs that are used up for a trade or business are going to be a deduction. The second group here, under a different internal revenue code, is called deductions for the production of income. This only applies to people, individuals like you and me. This could also apply to individuals, but also corporations. So this one doesn't apply to corporations. The main category here would be for rental operations, rental property being a landlord, and the costs you incur in running your rental units. The costs for rental operations will be deducted here under this section. Then there's other sections in the turnover of the code allowing other specific deductions, like itemized deductions that we'll see in this chapter but more so in a future chapter. And then maybe we talked about one called alimony maybe from...

Award-winning PDF software

Video instructions and help with filling out and completing Why Form 8453 S Deduction